Does a sole trader in Slovakia need a payment terminal?

Since 2026, many sole traders in Slovakia have been asking whether they must buy or rent a payment terminal. The answer is simpler than it may seem: the key issue is not necessarily the terminal itself, but the ability to offer a cashless payment option.

In short

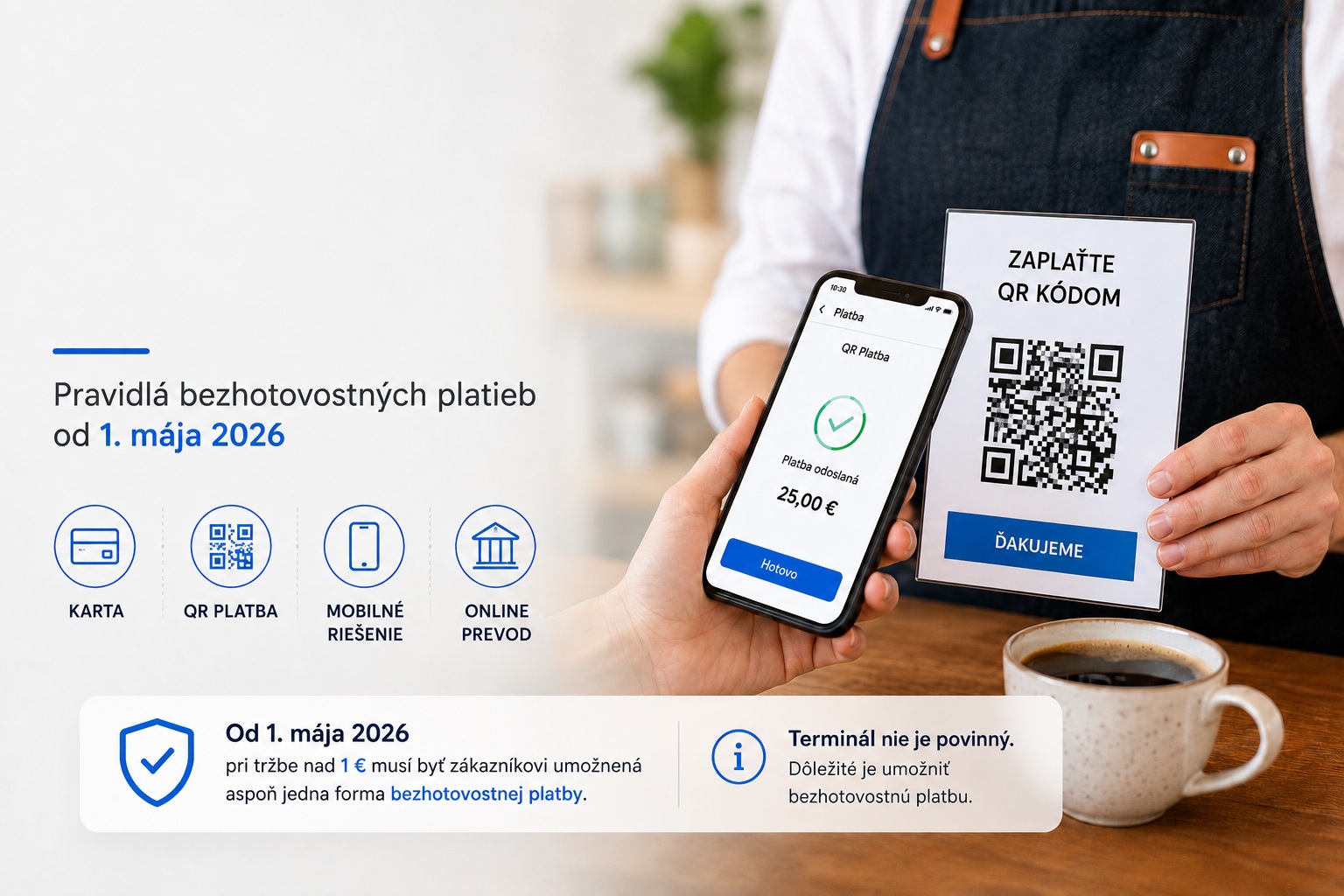

A sole trader in Slovakia does not automatically need a traditional payment terminal. However, if they accept sales at a point of sale and the obligation applies to them, from 1 May 2026 they must enable a cashless payment option for transactions above 1 euro. This may be a card payment, QR payment or another cashless method.

Why the question of payment terminals comes up

When people hear about mandatory cashless payments, many immediately imagine a traditional card terminal on the counter. We know it from shops, restaurants and petrol stations. The customer taps a card, phone or smartwatch, and the payment is completed within seconds.

But a sole trader often works differently from a large business. They may work in the field, visit customers, provide services at a client’s home, sell at markets or process only a few payments per day. For this type of business, a traditional terminal may not always be the most practical or cost-effective solution.

That is why it is important to distinguish between two things: the obligation to enable a cashless payment and the obligation to have a specific payment terminal. These are not the same.

Does a sole trader need a terminal?

In general, a sole trader does not automatically need a traditional payment terminal. What matters is whether the customer can pay cashlessly when the legal obligation applies to that transaction.

In other words: the rules are not only about having a specific device on the counter. They are about whether the buyer has a real possibility to pay without cash. This can include a card payment, QR payment, online bank transfer or another cashless method.

The difference between a terminal and a cashless payment

A payment terminal is only one tool. A cashless payment is a broader concept. It includes several payment methods where the customer does not pay with physical cash, but electronically.

- a terminal is suitable mainly for frequent card payments,

- a QR payment may be simpler for smaller businesses or field services,

- mobile solutions may be practical when the sole trader does not have a fixed business location,

- an online transfer may make sense for certain types of services.

Important note

The right question is not only “Do I need a terminal?”, but rather “Can I offer the customer at least one working cashless payment option?” If the answer is yes, a traditional terminal does not have to be the only possible solution.

Who is affected by the obligation

The obligation to enable a cashless payment mainly concerns sellers who accept sales at a point of sale and register them under the rules for sales registration. From 1 May 2026, for transactions above 1 euro, the buyer should also be able to pay cashlessly.

For a sole trader, it is therefore important to first look at whether their specific activity involves accepting sales in a way that is subject to sales registration. Not every sole trader operates in the same way. A craftsman working at a customer’s home, a hairdresser, a market seller and a business invoicing services exclusively by bank transfer may all be in different situations.

If a business owner is unsure, the most sensible approach is to check their specific situation with the current rules of the Financial Administration or with an accountant. With this type of obligation, the practical way in which sales are accepted, recorded and documented often matters.

What options exist without a terminal

If a sole trader does not want or does not need a traditional payment terminal, there may still be several options. The important thing is that the method is clear, usable for the customer and allows the business owner to identify the payment correctly.

QR payment

With a QR payment, the customer scans a QR code with their phone and completes the payment in their banking app. The advantage is that the customer does not have to manually copy the IBAN, amount or variable symbol if these details are correctly included in the QR code.

Mobile payment solution

Some solutions allow businesses to accept payments through a mobile phone or application. For services in the field, this may be more practical than carrying a separate payment device.

Payment terminal

A terminal can be the most convenient option where customers often pay by card or mobile phone. For a stable business with a higher number of daily payments, it can be very practical. However, it is not automatically the only option for every sole trader.

Online bank transfer

For some types of services, the customer may pay by online bank transfer. In this case, it is important to consider the speed of confirmation, correct payment identification and the practical process for delivering the goods or service.

Practical example

Imagine a sole trader who provides repair services at customers’ homes. They process only a few payments per day and do not want to use a traditional terminal. After the service is completed, the customer says they do not have cash. In such a situation, it is useful to have a simple cashless procedure ready.

| Situation | Problem | Solution |

|---|---|---|

| The sole trader completes a service at the customer’s location | The customer does not have cash | The business owner offers a QR payment or another cashless option |

| The customer wants to pay by card | The sole trader does not have a terminal | If another working cashless option is available, a terminal may not be the only solution |

| The payment must be identifiable | Without a reference or note, payment matching becomes harder | A QR code can include the amount, IBAN and payment identification details |

For a small business, such a solution may be simpler than immediately investing in a terminal. At the same time, the customer does not leave with the feeling that payment is complicated.

What to watch out for

The biggest mistake is thinking that simply telling the customer a bank account number is enough. In practice, the payment process should be clear, quick and easy to match later.

Recommended

Prepare a cashless payment method in advance, test it, use clear payment identification and keep the process simple for both the customer and the business owner.

Watch out for

Do not rely on a solution that cannot be used quickly in practice. Problems may occur with weak internet, missing payment confirmation or an unclear variable symbol.

Cash is not being abolished

The obligation to enable a cashless payment does not mean that cash is disappearing. Customers can still pay in cash. The new rules mainly expand payment options so that customers are not limited only to cash.

For a sole trader, this can also be an advantage. If a customer does not have cash, a cashless alternative can save the sale, the service or the customer experience. A good payment solution is therefore not only an obligation, but also a practical business tool.

Frequently asked questions

Conclusion

A sole trader does not need to panic and assume that a traditional card terminal must immediately be placed on the table. The important point is to understand that the obligation is aimed at enabling a cashless payment, not necessarily at using one specific device.

For some businesses, a terminal will be the best solution. For others, a QR payment or mobile solution may be simpler. What matters is that the payment is easy for the customer, verifiable for the business owner and practical in everyday use.

The best approach is to prepare before a problem occurs at the moment of payment. If the business owner can calmly tell the customer “you can also pay cashlessly,” it creates a more professional impression and lowers the risk that a sale remains unfinished.

Do you want to accept cashless payments more simply?

If you do not need a traditional payment terminal, a clear QR payment can be a practical option. The customer sees the amount and payment details, while you get better payment identification.

I want to try QR PAYMENT